Rent or Buy in Charlotte? The Honest Math

Charlotte-specific rent vs buy break-even math, property tax and insurance reality, and when each option wins.

How to think about Charlotte rent vs buy

Most online rent-vs-buy calculators give you a number that feels precise but ignores local market realities. Generic tools often miss critical factors like the specific 2026 property tax adjustments hitting Mecklenburg County. As a professional service team, we use a different framework to evaluate these decisions.

This guide walks through the exact inputs that actually matter for local homeowners and business owners right now.

For broader context, see our Home Buyer Services and Apartment Locating practices, plus our first-time home buyer guide for Charlotte for the closing-process basics if buying wins your math.

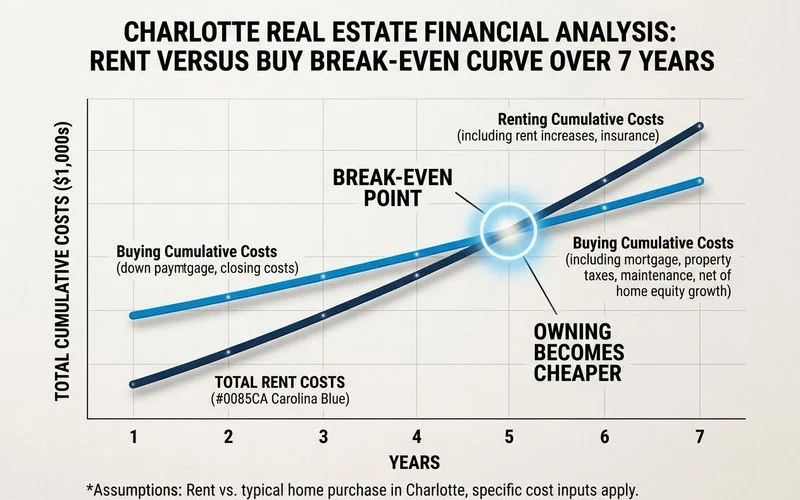

The Charlotte break-even math

The typical break-even point for renting versus buying a home in Charlotte currently sits at four to six years. This timeline depends heavily on current price-to-rent ratios across different zip codes.

We track these market statistics closely to provide accurate advice. Recent data from Canopy MLS shows the median home price in Charlotte hovering around $412,500 in the first half of 2026. This represents a normalization in the market, making the math slightly different than the explosive years of 2021 and 2022.

The baseline four to six year window rests on a few core assumptions for the current year:

- A 6.4% to 6.5% average mortgage rate, based on recent Freddie Mac reports.

- A 3% to 4% annual home-price appreciation rate projected by major real estate analysts.

- A steady 2% to 3% annual rent inflation rate.

- A standard 20% down payment on a median-priced property.

- The Mecklenburg County property tax rate, which sits around 0.80% effective.

If you plan to stay less than four years, renting usually wins regardless of the neighborhood. Business owners and transient professionals often benefit from this short-term flexibility. Buying typically wins out if you plan to stay for seven years or more.

The middle window of four to seven years is where the decision becomes highly nuanced.

Property tax and insurance reality

Owning property in Charlotte requires budgeting for local taxes and rising insurance premiums. The Mecklenburg County effective property tax rate runs about 0.80% on residential property. This ongoing expense is a highly meaningful factor for the buy-side math.

The county manager proposed a rate increase in the 2026 budget to cover civic projects and infrastructure. This adjustment means you need to calculate costs accurately based on current property values.

| Charlotte Home Value | Estimated Annual Property Tax | Estimated Monthly Tax |

|---|---|---|

| $412,500 (2026 Median) | $3,300 | $275 |

| $600,000 | $4,800 | $400 |

| $800,000 | $6,400 | $533 |

Insurance costs are also shifting across North Carolina. The state insurance commissioner recently negotiated a 7.5% average rate increase for homeowners policies effective in 2025.

Another 7.5% increase takes effect in June 2026. A typical Charlotte policy now runs $1,500 to $2,500 a year, with exact figures depending on the home’s age and specific location.

Our team advises clients to always factor in Homeowners Association fees. These HOA dues often run $80 to $300 a month for newer construction or condo properties. The all-in monthly cost of a median $412,500 Charlotte home with 20% down at a 6.5% rate is roughly $2,080 for Principal and Interest.

Adding $275 for taxes and $150 for insurance brings the total to around $2,505 per month before any maintenance.

Comparing that $2,505 mortgage to a $1,900 average South End apartment reveals a $605 monthly gap. The buy-side gets you forced savings through equity over time, while the rent-side gets you immediate cash flow flexibility.

When renting first makes sense

Several specific lifestyle and financial scenarios genuinely favor renting over buying. Choosing a lease can protect your capital while you finalize long-term plans.

You are new to the local market

Learning the different corridors and traffic patterns takes time. A year of renting in a lively area like South End or Plaza Midwood lets you learn the city.

You avoid locking into a 30-year financial decision before understanding the layout. For reference, recent 2026 data shows average apartment rents in South End sitting around $1,900.

You need to build cash reserves

Saving an extra 5% to 8% in down payment cash during a rental year strengthens your purchasing profile. Our preferred lending partners note that a larger down payment secures significantly better loan terms.

With average interest rates hovering in the mid-six percent range, extra cash directly lowers your monthly obligation.

Your timeline is uncertain

Career moves and business relocations often dictate a shorter stay. Job stability concerns or anticipated family changes within the next three years favor the flexibility of renting.

Exiting a lease is vastly cheaper than selling a home shortly after buying it.

Your neighborhood preference is unclear

Touring a neighborhood is completely different from actually living there. Spending a year in an apartment reveals the daily reality of grocery runs and commute traffic.

Actual life in a Charlotte corridor shows you what weekend tour days completely miss.

When buying immediately wins

Purchasing a home right away is the smartest choice when you possess a clear timeline exceeding five years and a stable income. The reverse cases for buying immediately rely on predictable life patterns.

Favorable terms and equity growth

Securing a known monthly cost protects you from annual rent hikes. Mortgage payments remain fixed for the life of the loan.

Our data highlights that Charlotte rents typically rise 2% to 3% annually, making a locked mortgage highly attractive over a ten-year horizon. Equity also compounds significantly over time.

Even a modest 3% appreciation on a $412,500 home outpaces typical rental savings strategies.

Scarce rental inventory in target areas

Finding a high-quality rental in specific residential submarkets is incredibly difficult. Desirable neighborhoods like Myers Park or Dilworth offer very limited rental inventory for larger single-family homes.

Buying might be the only realistic path if you require a specific school district or property size.

Stable income and known commute

Job stability heavily reduces the downside of a wrong-neighborhood decision. Business owners and established professionals with a predictable daily route benefit from securing a permanent base.

Buying allows you to optimize your housing location around a permanent office or business headquarters.

The Charlotte-specific factors

Three distinct local dynamics shape the Charlotte rent-versus-buy math more than in other national markets. These factors heavily influence the timeline for recovering your initial investment.

We evaluate these exact elements for every single client. Understanding these specific nuances prevents costly geographic mistakes.

- Neighborhood-driven variability: Walkable inner-loop neighborhoods like South End carry higher price-to-rent ratios, which extends the break-even timeline. Suburbs near Lake Norman or South Carolina border towns offer a shorter break-even period because local rents and purchase prices align more closely.

- Strong appreciation history: Charlotte home values continue to outpace the national average. The city added over 20,000 new residents recently, keeping housing demand very strong. While the explosive 5% to 7% growth of the past decade has slowed, steady 3% to 4% appreciation still heavily favors long-term buyers.

- Lower transaction costs: North Carolina closing costs are exceptionally favorable compared to coastal states. Local closing costs average roughly $2,480, or about 0.56% of the purchase price before large lender origination fees. This sits far below the 4% to 6% transfer taxes seen in places like New York or California.

Lower friction at the closing table means buyers recover their sunk costs much faster in Mecklenburg County.

What we recommend for relocators

The most reliable path for new residents is to rent for six to twelve months before buying a property. This approach provides necessary time to validate commute realities and neighborhood preferences.

We guide dozens of professionals through this specific sequence every single year. A structured timeline dramatically reduces stress and leads to better financial outcomes.

- Rent for a brief 6 to 12 month period upon arrival in a corridor you have shortlisted with our apartment locating service.

- Use the initial rental year to test your daily commute and build local context.

- Engage our home buyer services during months eight to ten of your lease to start a targeted buy-side search.

- Close on a new property roughly 12 to 15 months after arriving, fully equipped with direct neighborhood knowledge.

This pattern does not fit every single situation perfectly. Corporate relocations with limited temporary housing packages might require an immediate purchase.

Immediate buying also works well if your family situation demands instant stability and you are prepared for the commitment.

The most honest answer to the rent-versus-buy question is that it depends entirely on your timeline confidence. A short conversation with a local professional who knows the 2026 market beats relying on an algorithm.

Common questions

What's the typical Charlotte rent vs buy break-even point?

Should I rent first when I arrive in Charlotte?

Are Charlotte property taxes high?

Related guides

Buyer Agent vs. Dual Agency in North Carolina

How NC's agency disclosure works and why exclusive buyer representation usually serves the buyer better.

Buying a Home in Charlotte During a Corporate Relocation

How RMC involvement, employer-paid closing costs, and start-date sequencing change the Charlotte buying workflow.

Buying a Home Sight-Unseen in Charlotte

Virtual-tour standards, contingency clauses, and on-the-ground buyer-agent verification for sight-unseen Charlotte purchases.

Closing Costs in North Carolina: What to Expect

Real NC closing cost ranges (2-5%), excise tax, attorney-state process, and what sellers contribute.

Ready to explore Home Buyer Services?

A short conversation gets you a curated, lifestyle-first match.