What NC Closing Costs Actually Look Like in 2026

Real NC closing cost ranges (2-5%), excise tax, attorney-state process, and what sellers contribute.

What buyers actually pay for closing costs in North Carolina

We find that closing costs in North Carolina typically run 2% to 5% of your purchase price.

This range fluctuates based on your specific lender, loan type, and local property taxes.

A $400,000 home purchase will usually require $8,000 to $20,000 in cash just to finalize the paperwork.

Our team constantly reviews these estimates to help clients avoid last-minute surprises.

This guide breaks down every expense category so you can build a realistic budget.

You need accurate figures instead of relying on a flawed online estimator.

For broader context on the purchasing process, review our Home Buyer Services page and the first-time buyer guide.

The major buyer-side cost categories

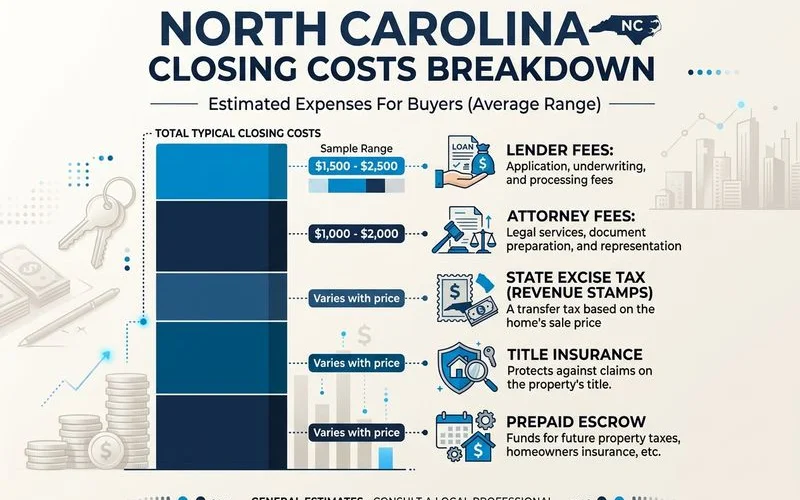

The bulk of your expenses fall into lender fees, title charges, local taxes, and prepaid escrows. These four categories account for the entire total.

Our typical clients see lender fees taking up the largest single chunk of change. Origination and underwriting charges cover the administrative work of processing your loan.

Lender fees

We suggest comparing Loan Estimates from multiple banks to find the best origination pricing. Total lender fees usually run 1% to 2% of the loan amount before any discount points.

- Origination fee: 0.5% to 1% of the loan amount.

- Discount points (optional): each point equals 1% of the loan, dropping your interest rate by roughly 0.25%.

- Appraisal: $500 to $700.

- Credit report: $30 to $100.

- Tax service fee: $50 to $100.

- Underwriting fee: $400 to $1,200.

Title and attorney fees (NC-specific)

Title insurance protects your ownership rights against past legal claims. Providers like Investors Title or Chicago Title issue these mandatory lender policies in the state.

Our preferred attorneys handle the extensive legal legwork required to clear the deed. Total title and attorney charges typically run 0.5% to 1.5% of the purchase price.

- Title insurance (lender’s policy, required): 0.3% to 0.6% of the loan amount.

- Title insurance (owner’s policy, optional but recommended): 0.3% to 0.5% of the purchase price.

- Closing attorney fees: $750 to $1,500.

- Title search and examination: $250 to $500.

State and local taxes

North Carolina charges specific transfer taxes whenever a property changes hands.

We see most local contracts default to the seller paying these specific revenue stamps. Buyers are still responsible for local recording charges.

- NC excise tax (revenue stamps): $1.00 per $500 of purchase price ($2.00 per $1,000). On a $400,000 home, that equals $800.

- Mecklenburg County recording fees: $80 to $200.

Prepaid escrow

Escrow accounts hold your funds to pay future property taxes and insurance premiums. These requirements vary widely by your closing month and total property value.

Our estimates usually allocate 1% to 2% of the purchase price for these prepaid items. Plan for 1% to 2% of the purchase price for prepaid escrows overall.

- Property tax: usually 2 to 6 months prepaid at closing.

- Homeowners insurance: 12 months prepaid (one full year).

- Mortgage insurance (PMI): partial month plus setup fees.

NC-specific items worth knowing

North Carolina requires an attorney to finalize real estate transactions and uses a unique due diligence structure. You will pay for title searches, deed preparation, and specific local transfer taxes.

We advise clients to review the standard North Carolina Offer to Purchase and Contract (Form 2-T). This standard form requires a non-refundable due diligence fee upfront. This fee is then credited toward your cash to close at the settlement table.

Excise tax (revenue stamps)

The state transfer tax ranks as one of the lowest in the country. A $500,000 home generates $1,000 in excise tax at the rate of $2 per $1,000 of the purchase price.

Our standard practice is to have the seller cover this cost, though you can negotiate the terms. You should confirm this detail during the initial offer stage.

Attorney-state closing

North Carolina sits among roughly a dozen states mandating attorney involvement in residential real estate closings. The closing attorney handles several vital legal steps to protect your investment.

- Title search and examination

- Deed preparation

- Closing document preparation

- Funds disbursement at closing

You select the closing attorney for the transaction. A listing agent might suggest someone, but you have no obligation to use their recommendation.

We encourage buyers to shop around since attorney fees remain completely negotiable. Local rates often vary by hundreds of dollars.

Property tax timing

North Carolina property taxes are paid in arrears on a calendar year basis. Counties typically mail the official tax bills in July or August.

The seller credits the buyer at closing for the portion of the year they owned the property.

Our clients then take responsibility for the full year’s tax payment when the bill comes due on September 1st. Taxes become legally delinquent if not paid by January 6th of the following year.

Sample closing-cost breakdown

A typical $400,000 home purchase in Charlotte generates roughly $10,400 in buyer fees. This equals about 2.6% of the purchase price when putting 20% down.

We created the table below to outline a standard scenario for a local buyer. This estimate requires a $320,000 conventional loan with a 6% interest rate.

| Category | Estimated Cost |

|---|---|

| Lender fees (1%) | $3,200 |

| Title insurance (lender + owner) | $2,400 |

| Closing attorney | $1,000 |

| Appraisal | $600 |

| Credit / underwriting | $1,000 |

| Property tax escrow (3 months) | $850 |

| Insurance prepaid (12 months) | $1,200 |

| Recording fees | $150 |

| Excise tax (typically seller pays) | $0 |

| Total buyer closing costs | ~$10,400 (~2.6%) |

This total does not include optional discount points. You should also subtract any seller concessions you successfully negotiate during the contract phase.

Lender vs third-party fees

Lender fees are negotiable origination charges, while third-party fees are fixed government and legal costs. You should compare Annual Percentage Rates to evaluate the true cost of different loan offers.

We often help clients decide whether they should pay higher upfront fees for a lower interest rate. Some lenders quote lower initial fees but compensate by charging higher monthly rates.

The Annual Percentage Rate includes both the interest rate and the required lender fees. You must also calculate the break-even point for any discount points you purchase. The typical break-even period for buying down a rate sits at five to seven years.

Our financial models show two distinct strategies based on your timeline:

- Staying 5+ years: Paying slightly higher upfront fees for a lower rate makes mathematical sense.

- Staying 3 to 4 years: Lower upfront fees usually win since you will not reach the break-even point on discount points.

When sellers contribute

Sellers can pay a percentage of your final expenses through negotiated concessions. Buyers in a balanced market can typically secure a 1% to 3% credit on conventional loans.

We see buyers successfully negotiate these credits during the initial offer or after the home inspection. These contributions reduce your out-of-pocket cash requirement at the settlement table.

The exact amount allowed depends entirely on your loan type and government regulations.

- Conventional loans: A 1% to 3% seller concession is common in the current Charlotte market.

- FHA loans: The Federal Housing Administration allows up to a 6% seller concession.

- VA loans: The Department of Veterans Affairs permits up to a 4% seller concession, plus additional VA-specific fees the seller can cover.

- USDA loans: Buyers can receive up to a 6% seller concession.

A seller’s willingness to contribute depends heavily on local market conditions and the days a property has sat on the market.

Our team finds that achieving a 1% to 3% seller concession is highly realistic on most homes in a balanced 2026 market like Charlotte. You just need a well-crafted offer.

What to ask about before closing

You must verify your final cash requirement and confirm property conditions seven days before settlement. Confirming wire instructions by phone and reviewing escrow setups will prevent last-minute delays.

We strongly advise checking three specific items a week before your scheduled closing date. Small misunderstandings at this stage can push back your entire timeline.

- Final cash to close. Your closing attorney will provide a Closing Disclosure with the exact figure, ideally three to five business days ahead of time. You must confirm wire instructions directly with the attorney’s office over the phone. Never trust wiring instructions sent via email. The FBI reports that real estate wire fraud costs buyers hundreds of millions of dollars annually.

- Property tax and insurance escrow setup. Your lender will confirm your specific escrow amounts and their effective dates. You need to understand exactly which months are prepaid and when your first normal mortgage payment is due.

- Walk-through findings. The final walkthrough happens 24 to 48 hours before closing. This critical step confirms the property is in the agreed-upon condition and any negotiated repairs are complete. If you spot missing repairs, you must address them before signing the papers.

You need a solid understanding of these details to ensure a successful transaction.

For a complete view of the purchasing timeline, read the first-time home buyer guide.

Our experts are always available to help you review your closing costs in North Carolina and build a secure financial plan.

Common questions

How much should I budget for NC closing costs as a buyer?

Is North Carolina really an attorney-closing state?

Can sellers cover my closing costs in NC?

Related guides

Buyer Agent vs. Dual Agency in North Carolina

How NC's agency disclosure works and why exclusive buyer representation usually serves the buyer better.

Buying a Home in Charlotte During a Corporate Relocation

How RMC involvement, employer-paid closing costs, and start-date sequencing change the Charlotte buying workflow.

Buying a Home Sight-Unseen in Charlotte

Virtual-tour standards, contingency clauses, and on-the-ground buyer-agent verification for sight-unseen Charlotte purchases.

First-Time Home Buyer Guide for Charlotte, NC

Pre-approval through closing. Charlotte's first-time buyer playbook with NC down-payment programs, contingencies, and pitfalls.

Ready to explore Home Buyer Services?

A short conversation gets you a curated, lifestyle-first match.