How Long Mortgage Pre-Approval Takes in Charlotte

Real Charlotte pre-approval timeline (1-3 days vs 1-2 weeks), what's required, why employment transitions complicate it.

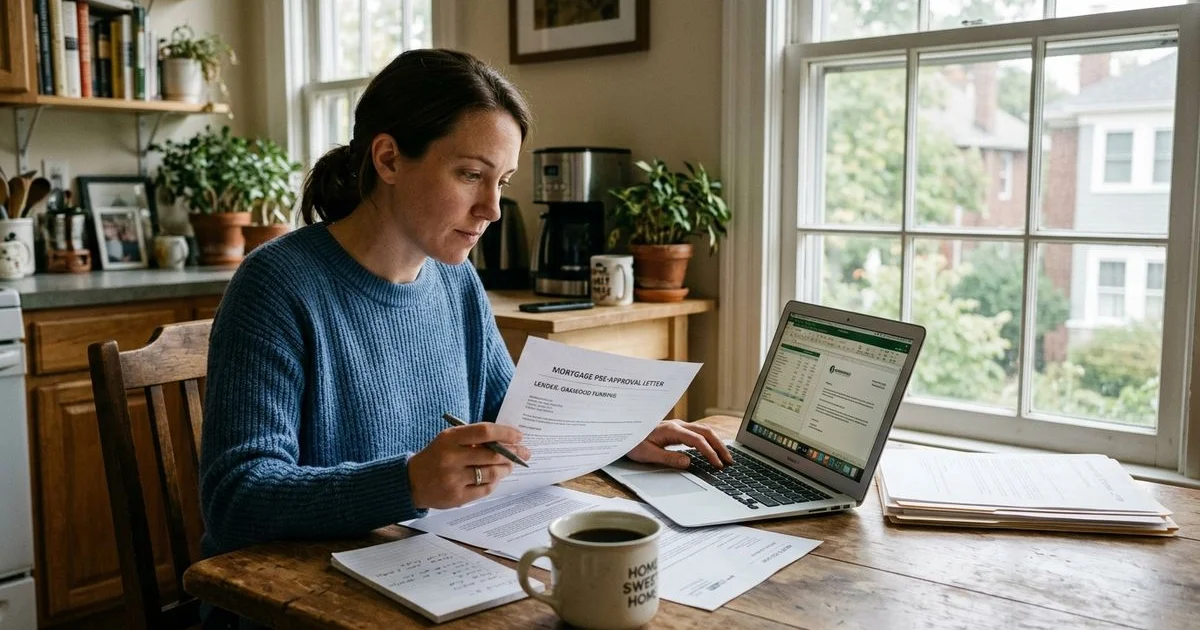

What pre-approval really tells a Charlotte seller

We often hear from knowledgeable professionals that securing a mortgage pre approval charlotte feels like a moving target in today’s market. Pre-approval serves as a loan officer’s preliminary commitment to a specific loan amount based on your documented income, credit, and assets.

It is definitely not just a basic credit pull. Our team sees a major shift in what Charlotte sellers expect in 2026.

A 680 credit score might get you in the door, but a verified pre-approval is the dividing line that separates standard offers from the winning bids.

This stronger version means your file has already passed preliminary underwriting. We know that with local median home prices around $427,000, presenting undeniable proof of funds is your best advantage.

The key takeaway here is that an automated underwriting system like Fannie Mae Desktop Underwriter has effectively stamped your file with a green light. Sellers want certainty.

Our goal here is to break down what this documentation requires, walk through the expected timelines, and address the specific quirks that affect relocators. For the broader buyer process context, see our Home Buyer Services page and the first-time buyer guide. Let us look at the exact steps you need to take right now.

What pre-approval requires

We require a standard package of financial documents to verify your income and assets. The typical charlotte mortgage lender package asks for two years of tax returns, recent pay stubs, and full bank statements.

This paperwork proves your financial stability.

Our underwriters use these documents to ensure you meet the 2026 conforming loan limit, which is currently set at $832,750 for Mecklenburg County. Lenders will pull your credit in parallel to check your FICO middle score across all three bureaus.

W-2 and Standard Income Employees

We look for consistency and clarity in your basic employment history. The standard package includes direct proof of your recent earnings.

- Two most recent W-2s and tax returns (1040 with all schedules)

- Two most recent pay stubs and a government-issued ID

- Two months of bank statements for all asset accounts

- Brokerage statements if pulling a down payment from investments

- Recent rent ledger if you are currently renting

Self-Employed and 1099 Applicants

Our process for business owners requires a deeper look into your cash flow. Underwriters are actively checking for large, unexplained deposits, which trigger mandatory review flags. Self-employed and 1099 applicants need specific documentation to prove stability.

- Two years of business and personal tax returns

- Year-to-date profit and loss statement

- Two months of business bank statements

- All relevant 1099 income documentation

We strongly advise separating your personal and business accounts well before applying. A messy commingling of funds is the number one reason files get delayed in underwriting.

Mortgage pre approval Charlotte: Typical timelines

We typically see the entire process taking anywhere from 24 hours to three weeks, depending entirely on your financial situation. A clean W-2 application with no missing pages moves rapidly through the system.

The single biggest delay is always documentation back-and-forth between the buyer and the loan processor.

Our team recommends setting up a shared digital folder to pre-stage your W-2s, tax returns, and bank statements before you even call a lender. Getting organized upfront cuts days off the standard pre approval timeline.

The 1-3 Day Path

We process clean W-2 applications with single incomes and established employment histories extremely fast. Modern digital portals allow us to verify assets electronically within hours.

- Day 1: Application submitted with complete documentation

- Day 2: Initial underwriter review

- Day 3: Electronic asset verification

- Day 4: Formal pre-approval letter issued

The 5-10 Day Path

Our timeline expands when we encounter multiple income sources, recent job changes, or restricted stock unit income. Verifying restricted stock units or tracking down human resources for an employment verification always adds a few days.

- Day 1: Initial application submitted

- Days 2-4: Documentation back-and-forth on income details

- Days 5-8: Verification of employment and stock vesting schedules

- Days 9-10: Final underwriter review and letter issuance

The 10-21 Day Path

We need significantly more time for buyers who are self-employed under two years, have complex business structures, or claim foreign income. These files require manual underwriting and often involve a CPA letter.

Multiple rounds of documentation requests are common in this tier.

Why employment transitions complicate things

We analyze your employment history to confirm that the income you are using to qualify will continue uninterrupted. A new job adds friction because it disrupts that track record. Most professionals relocating to North Carolina are coming for a new opportunity with major employers like Bank of America, Atrium Health, or Honeywell.

Our lenders need documented evidence that your new position is stable before they will approve the loan. Your debt-to-income ratio, which lenders typically cap around 43 percent, must be supported by verifiable future earnings.

How Different Transitions Affect Approval

We evaluate job changes based on the industry and the structure of your compensation. An internal corporate transfer is the easiest scenario because it is treated as continuous employment.

- Same-field, same-employer transitions: Easiest path, treated as continuous employment.

- Same-field, different-employer transitions: Easy if the offer letter states a clear start date and base salary.

- Field changes or industry switches: Slightly harder, requiring your first actual paystub from the new company.

- Self-employed to W-2 transitions: Usually fine because salaried income is easy to project.

- W-2 to self-employed transitions: Extremely hard, requiring a full 24 months of new tax returns.

Our best advice is to talk to a loan officer early if you are mid-transition. They can guide you on whether getting a letter before your actual start date is realistic for your specific situation.

Conventional vs. FHA vs. VA notes

We offer several distinct loan types, each designed for a specific buyer profile and down payment strategy. A conventional loan is the most common choice for buyers with strong credit scores over 700.

For sight-unseen buyers, all four primary loan types work in North Carolina.

Our local market data shows 30-year fixed rates hovering around 6.4 percent in early 2026. VA and conventional paths are usually the most relocator-friendly because their documentation patterns are highly predictable. This predictability takes a lot of stress out of an interstate move.

Loan Program Comparison

We use this baseline data to help clients compare their options side-by-side. The math usually favors a conventional product if you qualify. These limits dictate your maximum purchasing power.

| Loan Type | Minimum FICO | Minimum Down Payment | Mecklenburg 2026 Limit |

|---|---|---|---|

| Conventional | 620 (700+ ideal) | 3% to 5% | $832,750 |

| FHA | 580 | 3.5% | $541,287 |

| VA | 580 to 620 | 0% | No strict cap |

| USDA | 640 | 0% | Geographically limited |

Key Program Details

We recommend conventional loans for buyers with 5 to 20 percent down because the private mortgage insurance drops off automatically at 78 percent equity. FHA loans provide a critical gap for credit-constrained buyers, though the mortgage insurance premium is now permanent on most of those notes. Veterans have a massive advantage with VA loans.

Our military clients utilize this path for zero percent down, no private mortgage insurance, and highly competitive rates. The VA funding fee is the only real trade-off, but you can finance that cost into the total loan amount. Some edge counties outside the immediate Charlotte metro still qualify for USDA programs.

We often check the exact property address for USDA eligibility to see if this zero-down option applies.

Lender shortlist considerations

Building a strong lender shortlist gives you the advantage to find the absolute best rate and terms. The right financial partner for an in-state buyer is sometimes the wrong fit for a sight-unseen buyer dealing with cross-state employment.

Our team actively maintains a working list of professionals who close cleanly with relocators. You want options that cover full-service infrastructure, aggressive rate shopping, and flexible underwriting.

A good Charlotte network includes multiple types of institutions.

Building Your Vendor Roster

We recommend structuring your contacts to include four specific types of originators. Having these lined up ensures you can pivot quickly if one denies your file. This diversity is your safety net.

- One large national bank (Wells Fargo, Bank of America, Truist) for relationship pricing and full-service infrastructure.

- One independent mortgage broker who shops multiple wholesale lenders on your behalf.

- One local credit union (like State Employees’ Credit Union) for highly competitive regional rates.

- One relocator-friendly direct lender with specific experience handling corporate relocation packages.

Our clients frequently find that brokers can secure a lower interest rate, but direct lenders can sometimes underwrite a file in-house much faster. You should compare their average closing timelines during your initial consultation. Communication style matters just as much as the final decimal point.

Practical advice

We tell every prospective buyer to organize their finances long before they start browsing Zillow. The pre-approval letter typically expires after 60 to 90 days, so timing your application is crucial.

If your search runs longer than the letter’s validity, you will need to refresh the documentation.

Our standard guidance is to pull your own credit reports at least two months out to identify any reporting errors. Disputing a false collection account can move your FICO score 20 to 50 points in just a few months.

If you are 60+ days from buying:

We need you to place your file in a holding pattern while maintaining perfect financial behavior. Any major credit change right now could derail your approval odds. Lenders look for complete stability leading up to the application.

- Pull your free annual credit reports and address any errors.

- Avoid major credit changes (no new cards, no large balance shifts, no closing accounts).

- Stage your documentation in a shared cloud folder so a lender can process everything instantly when you are ready.

If you are 30-60 days from buying:

Our strategy shifts to immediate action once you cross the two-month threshold. Getting a hard inquiry on your credit report will cause a minor, temporary dip in your score. Multiple mortgage inquiries within a 14 to 45-day window count as a single event, so do not fear shopping around.

- Get formally pre-approved now, even before specific listings come into view.

- Confirm the total loan amount aligns perfectly with your realistic search range.

- Lock in a rate window if current rates are favorable and you are within 60 to 90 days of closing.

We encourage you to secure your mortgage pre approval charlotte early to ensure you have the buying power you need. Your real estate agent will need this document before submitting any formal offers. Reach out to a verified Charlotte mortgage lender today to start your application and get your financial profile fully verified.

Common questions

How fast can I get pre-approved in Charlotte?

Do I need pre-approval before touring Charlotte homes?

Does a new job complicate pre-approval?

Related guides

Buyer Agent vs. Dual Agency in North Carolina

How NC's agency disclosure works and why exclusive buyer representation usually serves the buyer better.

Buying a Home in Charlotte During a Corporate Relocation

How RMC involvement, employer-paid closing costs, and start-date sequencing change the Charlotte buying workflow.

Buying a Home Sight-Unseen in Charlotte

Virtual-tour standards, contingency clauses, and on-the-ground buyer-agent verification for sight-unseen Charlotte purchases.

Closing Costs in North Carolina: What to Expect

Real NC closing cost ranges (2-5%), excise tax, attorney-state process, and what sellers contribute.

Ready to explore Home Buyer Services?

A short conversation gets you a curated, lifestyle-first match.